Long-Term Investing: Your Shield Against Market Volatility

Long-term investing is one of the easiest and most reliable ways to build wealth and protect your money from market ups and downs. Instead of trying to time the market or chase short-term profits, long-term investing focuses on staying invested and letting your money grow over time through compounding and market recovery.

If daily stock market news makes you nervous, you’re not alone. But with a long-term plan, you can avoid stress and focus on growing your money the smart way. Here’s why time is your best friend in investing.

The Power of Time in Investing

Time is your biggest ally when it comes to building wealth. The Indian stock market, tracked by the Nifty 50, has averaged ~12% annual returns since 1995, despite crashes and corrections. Globally, the S&P 500 has delivered ~10% annually since 1928. This growth comes from compound interest—your returns earn returns, creating a snowball effect.

Example of Compound Growth

| Years Invested | Initial Investment | Value at 10% Annual Return |

|---|---|---|

| 1 | ₹10,000 | ₹11,000 |

| 5 | ₹10,000 | ₹16,105 |

| 10 | ₹10,000 | ₹25,937 |

| 20 | ₹10,000 | ₹67,275 |

| 30 | ₹10,000 | ₹1,74,494 |

Why It Matters: Starting early and staying invested unlocks exponential growth, turning modest sums into significant wealth.

Also Read :- HOW INFLATION IMPACTS YOUR FINANCES & HOW TO PROTECT IT

Reducing Risk with Longer Horizons

Short-term market dips can be nerve-wracking, but a long-term approach slashes risk. Historical data shows that the longer you hold investments, the lower the chance of losing money:

| Holding Period | Probability of Positive Returns | Chance of Loss |

|---|---|---|

| 1 Year | 74% | 26% |

| 5 Years | 88% | 12% |

| 10 Years | 94% | 6% |

| 20 Years | 100% | 0% |

Key Insight: Over 20 years, major indices like the Nifty 50 or S&P 500 have never delivered negative returns historically, thanks to market recoveries.

Volatility: Your Opportunity, Not Enemy

Market corrections (5-20% drops) and bear markets (20%+ drops) are normal but temporary. They’re opportunities to buy at lower prices if you’re a long-term investor.

- Minor Corrections: Happen yearly, recover in ~3 months.

- Major Corrections: Occur every 2 years, recover in ~8 months.

- Bear Markets: Every 7-10 years, with a 100% recovery rate.

Missing the market’s best days—often right after the worst—can halve your returns. For example, staying invested during the 2008 crisis (51% Nifty drop) led to a 74% rebound in 2009.

Tip: Hold steady during dips to capture full recovery gains.

Also Read :- Mastering Patience: The Key to Investment Success

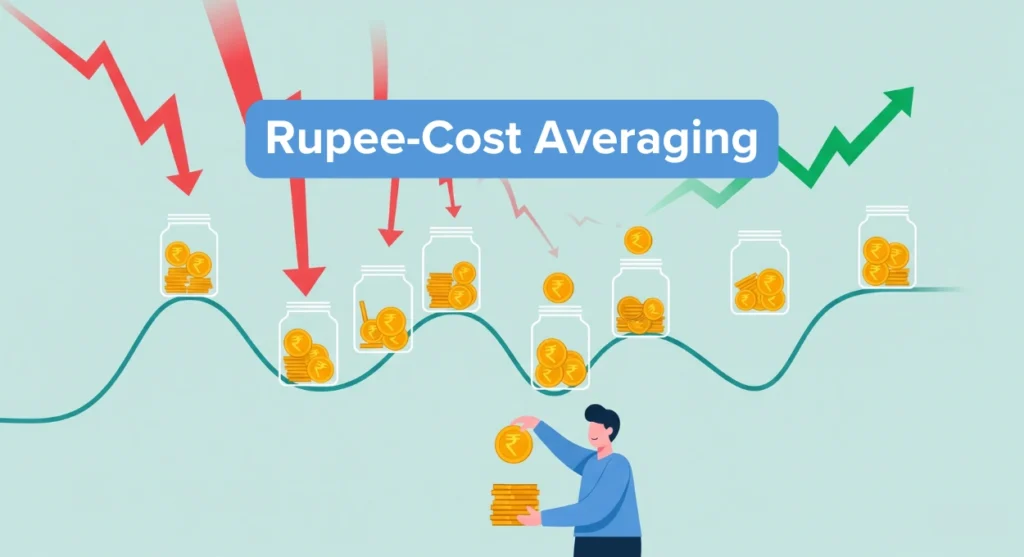

Rupee-Cost Averaging: Taming Volatility

Worried about investing at a peak? Rupee-cost averaging —investing a fixed amount regularly, like ₹5,000 monthly via a Systematic Investment Plan (SIP)—smooths out volatility.

How Rupee Cost Averaging Works

- Market Dips: Buy more units at lower prices.

- Market Peaks: Buy fewer units at higher prices.

- Result: Lower average cost per unit over time.

Benefits

- Discipline: Avoids emotional decisions.

- Cost Efficiency: Reduces average purchase price.

- Consistency: Builds wealth steadily.

Example

| Monthly Investment | Annual Return | 20-Year Value |

|---|---|---|

| ₹5,000 | 12% | ₹23.2 lakh |

Tip: Automate SIPs to stay consistent and stress-free.

Also Read :- Avoiding Portfolio Over-Diversification: Smart Strategies for Investors

Beating Inflation with Equities

Inflation eats away at your money’s value—₹100 today might buy only ₹95 next year. Equities are your best shield, historically outpacing inflation. The Nifty 50’s nominal return (~12%) translates to 8-9% after ~3% inflation, while fixed deposits often lag.

| Asset Class | Nominal Return | Real Return (After 3% Inflation) |

|---|---|---|

| Equities | 12% | 8-9% |

| Fixed Deposits | 6% | 2-3% |

Why Equities Excel: Companies grow revenues and earnings, adjusting to rising costs, unlike fixed-income assets.

Diversifying for Resilience

A diversified portfolio across asset classes reduces risk while maintaining growth potential. Modern Portfolio Theory shows that combining assets with different behaviors lowers volatility.

Suggested Allocation

| Age Group | Equities | Fixed Income | Real Assets (REITs, Commodities) |

|---|---|---|---|

| 20-30s | 70-80% | 15-20% | 5-10% |

| 40s | 50-60% | 30-40% | 5-10% |

| 50s+ | 30-40% | 50-60% | 10% |

- Equities: Drive growth and inflation protection.

- Fixed Income: Add stability, especially near retirement.

- Real Assets: Hedge inflation and diversify.

Tip: Rebalance annually to keep your allocation on track.

Also Read :- Are You Overdiversifying? The Hidden Risks of Too Many Index Funds for Indian Investors

The Buy-and-Hold Edge

Buy-and-hold—buying quality assets and holding them for years—maximizes returns with minimal effort.

Advantages

- Cost Savings: Fewer trades mean lower fees and taxes.

- Tax Efficiency: Long-term capital gains in India are taxed at 12.5% (above ₹1.25 lakh), vs. 20% for short-term.

- Simplicity: Less time monitoring markets.

- Emotional Ease: Avoids panic-selling during volatility.

Example

A ₹1 lakh investment in a Nifty 50 index fund in 2005, held for 20 years at 12% returns, would be worth ₹9.65 lakh today.

Tip: Opt for low-cost index funds or ETFs for easy buy-and-hold.

Mastering Your Emotions

Investing tests your emotions. Common traps include:

- Loss Aversion: Selling during dips to avoid losses.

- Recency Bias: Chasing recent winners or fleeing losers.

- Market Timing: Trying to predict highs and lows.

Solution: Stick to a systematic plan like SIPs and focus on long-term goals to bypass emotional pitfalls.

Your Long-Term Investing Plan

Ready to start? Here’s a simple framework:

- Set Goals: Define retirement, education, or wealth targets.

- Assess Risk: Gauge your comfort with market swings.

- Allocate Assets: Build a diversified portfolio based on age and goals.

- Invest Regularly: Use SIPs or auto-investments for consistency.

- Stay Disciplined: Rebalance yearly, ignore short-term noise.

Also Read :- Goal-Based Financial Planning: Your Personal Roadmap to Financial Freedom

Conclusion

Long-term investing is your shield against market volatility and a proven path to wealth. By harnessing time, compounding, and diversification, you can turn market fluctuations into opportunities. Whether through Rupee-cost averaging, buy-and-hold, or a balanced portfolio, the key is patience and discipline. Start today, stay the course, and watch your wealth grow over time!

FAQs (Frequently Asked Questions)

1. Does long-term investing reduce risk?

Yes, historical data shows a 100% chance of positive returns over 20 years, as markets recover from downturns.

2. What is compound growth?

It’s when your investment returns earn returns, leading to exponential wealth growth over time.

3. How does Rupee-cost averaging help?

RCA involves regular investments, lowering average costs and reducing the impact of market volatility.

4. How do equities protect against inflation?

Stocks grow faster than inflation (8-9% real returns), preserving purchasing power unlike fixed deposits.

5. What is asset allocation?

It’s spreading investments across equities, bonds, and real assets to balance risk and return.

6. How does buy-and-hold work?

Buy quality assets and hold them long-term to minimize costs, taxes, and emotional decisions.

7. How do I avoid emotional investing mistakes?

Use systematic plans like SIPs and focus on long-term goals, not short-term market swings.

Disclaimer :- This blog is for informational purposes only and does not constitute financial or investment advice. Investing involves risks, including potential loss of principal. Past performance is not indicative of future results. Consult a financial advisor and conduct your own research before investing. Data is sourced from publicly available information as of August 4, 2025, and may change. The author and publisher are not liable for any financial losses resulting from decisions based on this analysis.